🔥 Save unlimited web pages along with a full PDF snapshot of each page. Unlock Premium →

Summary

Alphabet's Google Cloud segment continues to grow, recording ~$4B in sales in the most recent quarter; but the business remains unprofitable.

Nonetheless, Google Cloud could achieve a ~$20B annual run rate by the end of FY '21 and is closing the gap with key rivals AMZN and MSFT.

I argue that Alphabet's current share price may assign little value to the Google Cloud segment, and thus current share prices may actually be undervalued as a result.

Based on my analysis, Class A GOOGL shares, at the moment, may be trading 10%-15% below a price that reflects a fair value of the Google Cloud business.

da-kuk/E+ via Getty Images

Still Playing Catching Up

Alphabet's (GOOGL, GOOG) Google Cloud business has come a long way since its early AppEngine-centric beginnings in 2008.

Revenue in Q1 FY '21 stood at $4.047B versus $2.777B in Q1 FY '20, jumping 46%.

The total loss for the business segment improved to ($974M) versus ($1,730M) in the prior year period. Using the sales data above, the efficiency of the business segment is noted to have improved considerably, losing ($0.24) per dollar of sales in the most recent period versus ($0.62) per dollar of sales in the prior year period.

The business could approach ~$20B in FY '21 if the company can maintain its recent average sequential quarter-over-quarter growth rate of ~10%.

Although, as Google Cloud remains in the red, heavyweights Amazon (AMZN) and Microsoft (MSFT) continue growing their respective cloud businesses' profitably and rather impressively. Amazon recently noted in their Q1 FY '21 earnings release that "[in] just 15 years, [Amazon Web Services ("AWS")] has become a $54 billion annual sales run rate business competing against the world's largest technology companies, and its growth is accelerating – up 32% year over year." Comparably, Microsoft's Intelligent Cloud segment recorded a 23% jump in QoQ revenue in Q3 FY '21, bringing in $15.1B, which in turn implies an annual run-rate in excess of $60B. Of course, the results of these three competing cloud businesses cannot be compared on an apples-to-apples basis due to their varying, and in certain cases questionable, compositions. However, the thrust of the preceding data, as readers already know, is that Alphabet is playing catch-up in the cloud.

Figure 1: Magic Quadrant for Cloud Infrastructure and Platform Services:: Google Is a Leader But Still Playing Catch-Up to AMZN and MSFT

With this in mind, I suggest in this report that investors may be:

Discounting Google Cloud's growth potential.

Subsequently undervaluing Alphabet's stock price as a result.

Basically, I argue that Alphabet's current share price may essentially associate little value toward the Google Cloud business. And, for that reason, shares may be trading at a bit of a discount to some fair value, to be derived later in this report. Please note that Google shares, as other analysts argue, may not correctly reflect the firm's overall growth potential; but, I am concerned here with a narrower perspective – that of the company's cloud segment and what "fully-valued" shares should be worth right now if the segment is assigned a "fair" value.

In the following sections, I layout my ideas. As is often the case when I write about Alphabet, when discussing the firm itself, I sometimes use "Google" and stock symbol "GOOGL" as synonyms for Alphabet. It should be clear to readers, based on context, when I am using "Google" and "GOOGL" from an organizational perspective. Additionally, readers will note that when discussing the stock itself, I make specific reference to the Class A GOOGL shares; although, the general ideas presented herein apply to the other shares classes as well (obviously).

Growth Potential

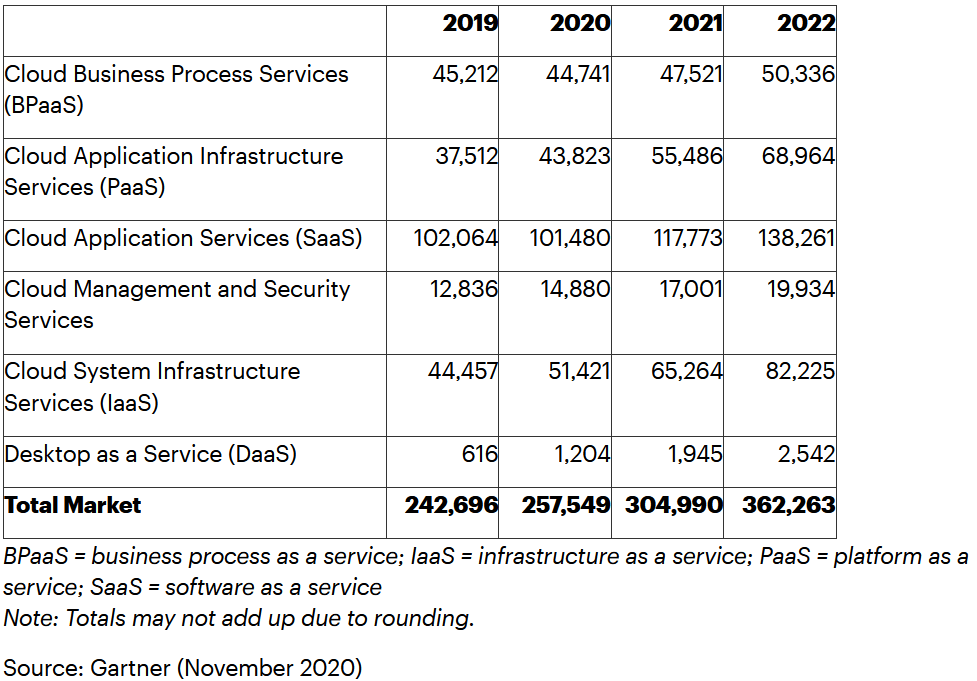

Before jumping into a quantitative analysis of my argument that Google's share price does not reflect an appropriate value for the cloud business, let us first consider the firm's opportunity in the cloud market. A Microsoft executive offered a "mouth-dropping" cloud market TAM forecast of $4T not too long ago. While MSFT's prediction may be a bit "aggressive", especially when considering that the figure exceeds all expected information technology spending in 2021, it may not necessarily be wrong. But either way, and as we all already know, the cloud (as a market) is big... very big with Gartner estimating total spend exceeding $300B in 2021, representing growth of 18% over 2020. Accordingly, despite AMZN's and MSFT's dominant positions, an abundance of space exists for GOOGL (and other players) to grow their cloud segment.

Figure 2: Worldwide Public Cloud Services End-User Spending

Naturally, Google's opportunity in the cloud should be considered in terms of those drivers catalyzing cloud market growth overall, and how the company's particular capabilities map to those drivers. Google CEO, Sundar Pichai, offered that "...there are three distinct market trends shaping [Google's] growth [in the cloud] and driving... product and go-to-market strategy" during the company's recent Q1 FY '21 earnings call. I summarize these trends and discuss them in the context of Google's offerings as follows:

1. Businesses are thirsting for increasingly sophisticated data analytics. Mr. Pichai notes "[Google's] expertise in real-time data and analytics is winning [data-heavy] companies like Twitter (TWTR) and Ingersoll Rand (IR), who are moving their complex data workloads to Google Cloud." This result is unsurprising. As I discussed in a previous Seeking Alpha article discussing Google and Snowflake (SNOW) in a data warehousing context, Google pioneered, more than a decade ago, "interactive-speed" analysis of massive-scale datasets via its Dremel technology, which subsequently evolved into the company's current cloud-based BigQuery offering. It is predictable, then, that Google is benefitting from data-driven trends in cloud computing. Further, as I also pointed out in the afore mentioned Seeking Alpha article, Google is a leader in artificial intelligence ("AI"), and particularly machine learning ("ML") technologies; technologies which are increasingly utilized by organizations to glean additional insights from data beyond the reach of traditional business intelligence ("BI"), as well as to support the data-driven development of new systems and products. Mr. Pichai accordingly points out the firm's success in analytics-related cloud projects is due to "[Google's] strength in AI and ML." Of perhaps all the trends pushing Google's cloud business forward, data analytics may be the most important as "[the] game is about data acquisition. The more corporate data that resides in a cloud the more sticky the customer is to the vendor."

2. Growth in infrastructure-as-a-service ("IaaS") projects. Google offers that they are winning important IaaS projects as large customers, in some cases, move entire data centers to the Google Cloud Platform ("GCP"), seeking the cost efficiencies and other benefits of cloud-based deployments. Moreover, in the firm's Q1 FY '21 earnings transcript, Mr. Pichai highlights the company's ability to support customers' hybrid and multi-cloud operations as a "true differentiator", enabled by technologies such as Google Anthos. On this point, GOOGL, like AMZN and MSFT, is pushing to offer organizations the tooling required to support complex applications that may operate across a variety of cloud and on-premise environments. Even Google BigQuery, mentioned earlier, has moved to a model where its engine supports massive-scale analytics – via its Omni offering – across datasets that are distributed across multiple cloud platforms. In other words, Google BigQuery Omni "...[empowers people] to access and analyze data, regardless of where it is stored." Although, despite these examples of Google Cloud technologies moving in the right direction, "...multicloud deployments are increasingly a two-cloud race between AWS and Microsoft Azure" at the moment. To reiterate the point from the introduction, Google is playing catch-up.

3. Software-as-a-Service ("SaaS"), the "original" cloud use case, remains a driver of cloud growth. As seen in Figure 2, Gartner forecasts the SaaS sub-market a bit shy of $120B in 2021, with an expected growth rate of 17% in 2022. It is the largest cloud sub-market where Google Workspace, inclusive of the company's popular Gmail, Meet, Sheets, and Docs offerings, appears to be thriving. Likely riding the remote work tailwind provided by the pandemic, Mr. Pichai highlighted "...[growth in Google Workspace's] revenue per seat and the number of seats in the last quarter." From a longer-term perspective, Google Workspace appears well-positioned for growth as the remote work and hybrid work trends continue to gain traction; and as organizations, in some cases, seek an alternative to Microsoft Office. Additionally, "[cloud] providers are [increasingly] going vertical to corner industries". It would be logical for Google to differentiate itself, as it already is, through industry-specific Google Workspace solutions. Certainly, a set of full-stack (IaaS, PaaS, SaaS) industry-specific solutions would likely prove very compelling for those organizations contemplating a move into the cloud.

Overall, the 3 market catalysts described above, alongside the company's technology stack, suggest Google has the ingredients to cook up an acceleration of growth of the cloud segment as they capitalize on these long-term trends. Without question, they face an uphill battle to match, much less surpass, the sheer size and scale of AWS and Microsoft Azure. But, consider:

Google itself already possesses a global computing infrastructure on par with the likes of AMZN and MSFT. Thus, the infrastructure to scale the Google Cloud business, arguably, already exists in large part; it is a matter of scaling the business which the company is trying to do, as evidenced by its more recent, aggressive hiring within the unit.

Google is closing the cloud capabilities gap with AMZN and MSFT (albeit perhaps not as fast as investors would like).

A growing and profitable Google Cloud business does not, obviously, have to compete with the heavyweights on every front. If, for example, Google can increasingly capture share of cloud analytics workloads, which as I suggested above may rest within a particular "sweet spot" relative to the company's historical capabilities and are especially valuable due to their "stickiness", such a dynamic could help put the firm into a position where "[cloud] operating results...benefit from increased scale", in turn driving profitability.

Indeed, the best is likely yet to come from Google Cloud...

Valuing Google Cloud

So, if we agree that Google is well-positioned in the cloud, if still trailing AMZN and MSFT, let us come back to my central idea of this analysis. My thought that investors may be discounting Google Cloud's growth potential centers on a simple observation derived from the firm's historical PE. Consider:

While there is no precise point in time at which one might say investors should have begun to "assign" a value to GOOGL's cloud business, perhaps we might – for my purposes here – say that the start of FY '12 marked a key turning point for Google Cloud as a commercial enterprise when, for example, AppEngine became an officially supported product and Google launched its Cloud Partner Program, among other developments.

When one examines the company's average PE before FY '12, the multiple is ~30. Interestingly, when one examines the company's average PE after FY '12 (ignoring the more recent run in the stock over the last few months), it is also ~30.

This simple observation certainly is not conclusive that investors are dismissing GOOGL's cloud segment. After all, it might be precisely what would be expected given that the business produces no earnings! However, this is Google after all; and it would not be unreasonable to anticipate some measure of PE multiple expansion relative to a maturing, even if still unprofitable, Google Cloud segment. Accordingly, from my point-of-view, it is suggestive that the firm continues to be largely valued on the basis of its legacy advertising and related businesses.

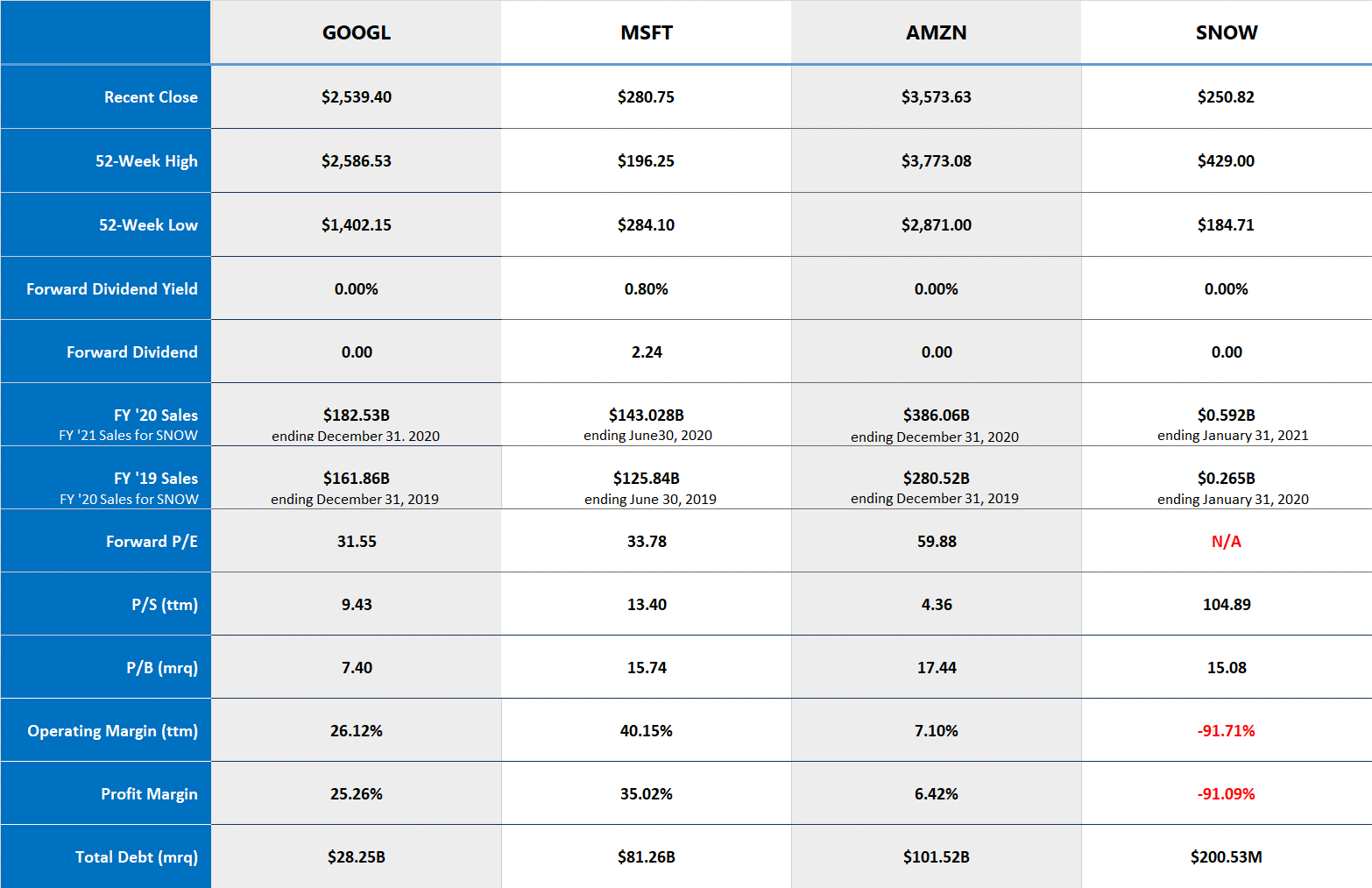

Perhaps the idea finds additional support when one considers the richer forward PE multiples of ~60 and ~34 for AMZN and MSFT respectively, as seen in Figure 3 below.

Figure 3: GOOGL and Selected Competitor Comparison

Data Source: Yahoo Finance

Table Source: Yves Sukhu

Notes:

Data as of market close July 16, 2021.

The higher PE multiples for AMZN and MSFT also do not allow us to conclude anything in an absolute sense; but, they could hint toward a broader investor community that currently places a greater value on their cloud businesses.

If my idea holds merit, the question is: "How much is the Google Cloud segment worth?"

It is not an easy question to answer obviously without more precise data. However, perhaps we can begin to sketch out a response with a consideration of the segment's quarterly revenue data.

From Figure 4, we can easily determine that the average sequential quarter-over-quarter growth rate of the business has been ~10% (as also mentioned in the introduction). Maintaining this rate over time, we can simply model cloud segment revenues through the end of FY '21 and subsequent fiscal periods.

Note that the revenue estimates in Figure 5 suggest GOOGL's cloud segment would exceed an annual run rate of $20B by Q4 FY '21, and $30B by Q4 FY '22. Now, using this data, let us assume:

Class A GOOGL shares are not grossly overvalued; an assumption which finds validation in MarketBeat's analyst consensus price target of $2513.20.

The Google Cloud segment will reach ~$19B in total sales (not annual run rate) at the end of FY '21, which is calculated by summing the actual Q1 FY '21 sales result with the Q2, Q3, and Q4 FY '21 estimates above.

Total shares outstanding at the end of FY '21 will be ~660M assuming the company reduces the total number of shares by ~1.5% via buybacks this year. Obviously, I don't know what the number will be; but this estimate seems possible.

With these assumptions in mind, we can calculate a cloud revenue/share forecast of $28.79/share in FY '21.

If we come back to my original suggestion that Google's current share price essentially assigns no value to the Google Cloud segment, what additional share value would be appropriate given the revenue/share forecast above? To answer this more refined question, we could apply an appropriate P/S ratio to arrive at a figure. If we were to "merely" apply Google's trailing-twelve-month ("ttm") PS multiple of 9.43, we would determine that the Google Cloud segment value is worth ~$271.50/share, suggesting that "Google Cloud-valued" Class A GOOGL shares are worth north of $2,800/share right now. But, is that multiple reasonable? Imagine, in some alternate reality, that the Google Cloud segment was a separate, independent entity at the moment. We see, again utilizing Figure 3, that SNOW – an unprofitable enterprise like Google Cloud – commands a PS multiple of ~105. Now, I have previously written about SNOW's valuation and I think SNOW's stock is overheated – to say the least; and so I don't think such a radical multiple should be applied to the Google Cloud segment. But, given that Google Cloud, AWS, and Microsoft Azure all overlap with SNOW's addressable market to – arguably – a large degree, it would seem reasonable that some multiple greater than the Google's current overall PS ratio would be more fair in the present market in a determination of the value of the segment. Indeed, if we were to argue that MSFT more closely resembles the Google Cloud business more than any other competitor in Figure 3, we could reasonably apply their PS multiple of 13.4 to establish a Google Cloud business value of ~$385.80/share, implying that "Google Cloud-valued" GOOGL shares are worth north of $2,900/share at the moment.

As always, we can push the numbers around any which way that we like. But, the general point, coming back to my declaration in the introduction, is that I think there is an argument to be made that GOOGL shares are undervalued right now due to investor dismissal of the cloud business, perhaps somewhere in the range of 10% - 15%.

Conclusion

MarketBeat's analyst data shows that a number of analysts boosted their price targets for the Class A shares in the general range of $2,800 - $3,000 over the last couple months. This target range obviously coincides well with the range that I derived in the previous section. Typically, I tend to lean a bit more to the conservative side when forecasting; but, my gut suggests to me that the Google Cloud segment is likely to power the stock over the long-term well beyond $3,000. I fully expect the "two-horse" cloud race between AMZN and MSFT to become a "three-horse" race in the not too distant future. I do think Google has struggled historically - for one reason or another - in terms of enterprise sales; and I think this, as opposed to any technological deficiency, may be their biggest weakness in a comparison against AMZN and MSFT. However, I, obviously, remain optimistic about their prospects. If an investor is seeking an undervalued cloud play, there may be no other better opportunity right now than Google.

This article was written by

I usually write to explore and articulate ideas that inform my own investment decision-making. So, typical...

Tech, Software, Long Only

Contributor Since 2017

I usually write to explore and articulate ideas that inform my own investment decision-making. So, typically, I am putting my capital where "my mouth is". I have a professional background in enterprise software, and I am presently working in a very niche area of computing. From time to time, I stray from the technology sector to write about companies that I think are worthy long-term investments.

Disclosure:I/we have a beneficial long position in the shares of GOOGL either through stock ownership, options, or other derivatives.I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

"Possibly" being 10-15% undervalued is hardly compelling these days. The error bars on any analysis must be larger than that.

@fusion150 - I understand your point, especially as it relates to a broader investor community that is increasingly focused on "large gain, short time-frame" type opportunities. That is my polite way of saying I think the broader investment community (not you personally) is increasingly looking for "get rich quick opportunities". And the opportunities that I see some investors piling into these days along that line appear incredibly dangerous to me. A 10% - 15% near-term upside in Alphabet shares may not seem all that compelling, but I believe -- as I argued in the report's conclusion -- that Alphabet is a long-term winner, with the cloud business likely serving as significant contributor to top-line and bottom-line growth as time goes on. I'll take 10% - 15% now (if my idea is right), and happily sit on the stock over the long-term. :-) Thanks for reading and commenting. Regards - Yves

Google is one of the best companies in the world.they would definitely be worth a lot more 10 or 20 years from now.the best performing faang stock in the last 5 years however is Apple.

In order to evaluate the potential revenue growth of GOOG cloud business, ine has to take in consideration what drives a customer to decide btw GOOG Cloud, AWS or Azure. The question is: since the addressable market is the same for these prominent players, what differentiates Google cloud from AMZN and MSFT offerings? Is there a comparison btw these three offerings?

@FcFr - agreed (re: in order to evaluate the potential revenue growth of GOOG cloud business, [one] has to take in consideration what drives a customer to decide btw GOOG Cloud, AWS or Azure.) And certainly there are any number of competitive comparisons available. I think areas where Google features an advantage include (1) massive-scale data analytics and (2) machine learning. This other article I wrote about Google and Snowflake makes reference to a Forrester report that also discusses Amazon and Microsoft, although the report is written in a data warehousing context: seekingalpha.com/...

You guy's apparently have a lot more money than I do to invest in a stock that pays no dividend and now "might" rise another 12% on an anti of $2,637 a share. When does the risk outweigh the reward? *10 share exposure talking.

@3carmonte when you survey top science and engineering graduates on where they want to work, google is always at the top. It's a great company. Their work in artificial intelligence cannot be discounted. When they blend this with the described analytics functionality the sky is the limit. Everyone will use it. Security is also a huge growth area for google and their cloud business. As hacks get more sophisticated cloud services will be required to do business and google has a massive loyal customer base that trusts them. That all means a lot of growth even if they stop trying. It's a money machine.

Agree, 10:1 split, IPO of 10-20 percent stakes of YouTube and Maps and GOOGL share price is off to the races. Management sees shareholders with disdain, only slowly improving since founders stepped down.

Coiled spring. I keep slowly adding.

MaritimeTrader

Google's cloud not profitable at this size. Is there structural issues to profitability such as low pricing or high cost vs comps (both larger like Amazon and Microsoft and smaller like Oracle). Maybe the market should value this business very low.

@dc10023 - I think Google expects to realize economies of scale as time goes on, and the data already points to that (i.e. loss per $ of revenue is decreasing). Also, don't forget -- perhaps more so in the case of Microsoft's Intelligent Cloud -- that companies "lump" in other stuff into their cloud businesses to juice the numbers. So, as I mentioned in the report, once cannot always make an "apples-to-apples" comparison between the heavyweight cloud vendors. Best - Yves

One more comment on $GOOGL... Hard to believe that the politicians on both sides of the aisle, most of whom have no idea about big business and the financial markets, are so hell bent on annoying these fine big tech companies. The politicians don't know what they're doing. These companies (GOOGL, AMZN, FB, MSFT) are the IBMs and GMs of fifty years ago. We are world leaders in tech and these companies have lead the economic success of our country over the last couple of decades. Why screw around with them? Just my two cents worth.

@esavela Agreed but you used the correct word in that the politicians are "annoying" the big tech companies. But I will bet that is all that will come of this saber rattling. Maybe even find a way to impose a "big" fine, as thought it matters, but no significant change if politicians like campaign contributions. And last time I checked, politicians like campaign contributions.

Is Google 10-15% undervalued on their cloud? Probably. I hear GCS come up more and more and they are actually trying to grow the business.

But

Litigation, government fines, broke governments, indebted governments could be understated.

Probably even worse than that is the risk of mass boycotts. I'm not saying it's going to happen but if they keep silencing voices and deleting videos, rigging search results the risk is north of 1%.

Long Google and I still think it's an add here.

@No Guilt - agreed that the potential impacts from government-related litigation should be on the radar of shareholders. In the end, I tend to think Google may be left alone...more or less. But, that's just my gut feeling. Best - Yves

@No Guilt mass boycotts by whom??????? As though there is or will be for the next 10 years a competitive search engine to Google for the right wing to support. How is the twitter and FB boycott progressing thus far? It's nothing more than right wing hot air by people who are full of hot air. But even the right wingers are as dependent on Google and big tech as everyone else. Do you realize that the Birmingham bus boycott lasted for 12 months? That is 12 months of blacks in Birmingham walking and carpooling, no matter the weather or time of day. You really think even 1% of the right wingers have anywhere near the intestinal fortitude or moral fiber to stop using big tech. Riiiiigth.

@ATLAtty Wow. What is Riiiiigth? don't underestimate the power of the silent majority.

$GOOGL is one of my high conviction holdings. I've been in it since $816/share. Always 100 shares or more so I can sell calls against it. The cloud is noted here in the article but I think the unlocked value is in YouTube and YouTubeTV. I understand that more internet bandwidth is used by traditional YouTube than by any other entity including streamers such as $NFLX. I personally would like to see a 10 for one split because as we all know, despite not adding any true value to the holder it does pump the stock price, invites more options activity, etc. And finally YouTubeTV--a totally different product is by far the best (IMHO) way to stream television. It is rather expensive but unlike all others, has unlimited cloud storage. Thanks for the article.

@esavela I agree on a split being desirable for exactly the reason you state--selling calls. I'll always own this as a core and won't risk assignment, but for trading I can stand to lose a few shares if called.

Author, your chart on end user cloud spending is great. Even if Alphabet never really competes with MSFT or AMZN in that arena, I'd think it is such an integral part now of youtube and other services that I'd prefer to keep building. I'll be watching earnings closely and hope for a dip, which is common for this one. Long GOOGL.

没有评论:

发表评论